In the contested airspace of the 21st century, surviving a mission depends as much on electronic awareness as it does on speed or firepower. Radar Warning Receivers (RWRs) sit at the heart of that awareness — silent, always-on sentinels that listen for the telltale emissions of enemy radar systems and alert pilots and crews before a weapon can be employed. As global defense spending surges, electronic warfare threats proliferate, and fifth-generation aircraft fleets expand, the Defense Radar Warning Receivers market is undergoing one of the most significant technological transformations in its history.

What Is a Radar Warning Receivers — and Why Does It Matter?

A Radar Warning Receiver is a passive electronic support measure (ESM) system designed to detect, identify, and alert operators to radar emissions that may indicate a threat — from ground-based surface-to-air missile (SAM) systems to airborne intercept radars aboard enemy fighters. Unlike active jammers, an RWR does not transmit; it listens. This passivity is precisely what makes it so valuable: it provides actionable intelligence without betraying the platform’s presence.

Modern RWRs operate across a wide frequency spectrum — typically from 0.5 GHz to 40 GHz or beyond — using sensitive antennas and onboard digital signal processors to compare detected emissions against stored libraries of known radar signatures. When a match is found, the system alerts the crew via audio cues, visual displays, or automated countermeasure triggers, enabling evasive maneuvers or the deployment of chaff and flares.

The criticality of RWRs extends far beyond fighter aircraft. Helicopters operating in low-altitude, high-threat environments depend on them for survivability. Transport and tanker aircraft — often unarmed and slow — rely on RWRs as a first line of defense. Unmanned Aerial Vehicles (UAVs), naval vessels, and even ground combat vehicles increasingly incorporate RWR technology as electronic warfare threats become ubiquitous across all domains of modern conflict.

From Crystal Video to Cognitive EW: The Evolution of Defense Radar Warning Receivers Technology

The story of Radar Warning Receivers begins in the Second World War, when crude crystal video receivers provided rudimentary detection of fire-control radars. Through the Cold War era, these systems grew considerably more capable, with analog superheterodyne receivers giving way to instantaneous frequency measurement (IFM) devices that could rapidly characterize an intercept without the need for slow frequency scanning.

The pivotal transition came with the shift to digital architectures in the 1990s and 2000s. Digital Radar Warning Receivers replaced analog signal processing chains with fast analog-to-digital converters and software-defined processing, dramatically improving frequency coverage, sensitivity, and — crucially — threat library management. Threat libraries, which store the parameters of known radar systems, became far larger and easier to update in the field, allowing operators to rapidly incorporate new emitter data gained from intelligence sources.

Today, the frontier of RWR development lies at the intersection of artificial intelligence, cognitive electronic warfare, and multi-sensor fusion. AI-assisted threat classification algorithms can now distinguish between closely related radar modes and identify previously unknown emitters by pattern recognition rather than simple library look-up. Cognitive EW systems go further still, enabling platforms to autonomously adapt their detection strategies and countermeasure responses based on the electromagnetic environment they encounter — learning and evolving in real time.

Multi-sensor fusion has also become a defining trend. Rather than processing radar emissions in isolation, next-generation systems correlate RWR data with inputs from missile approach warning systems (MAWS), laser warning receivers (LWRs), and electro-optical sensors to build a unified, geo-located threat picture. This integration of capabilities — frequently packaged under the umbrella of a Defensive Aids Suite (DAS) — represents the operational standard that major air forces are now demanding.

Key Market Drivers Shaping the Defense Radar Warning Receivers Market

Rising Defense Budgets and Electronic Warfare Prioritization

Global defense expenditure reached record levels in recent years, with NATO members increasing EW investment substantially following lessons observed from conflicts in Ukraine, Syria, and the South Caucasus. Peer and near-peer adversaries — China and Russia chief among them — have invested heavily in advanced integrated air defense systems (IADS), making the ability to detect, characterize, and defeat radar emissions a top-tier survivability requirement. This has translated directly into increased procurement and upgrade programs for RWR systems across virtually every platform category.

The Fifth-Generation Fighter Expansion

The expansion of fifth-generation fighter fleets — led by the F-35 Lightning II and complemented by the emerging development of sixth-generation programs — has created a high-value market for fully integrated, software-defined EW suites. Fifth-generation platforms demand RWR systems that are seamlessly fused with onboard sensors, capable of passive tracking, and designed to exploit low-observable apertures. The F-35’s AN/ASQ-239 Electronic Warfare System, developed by BAE Systems, exemplifies this approach: a comprehensive suite that blends radar warning, geolocation, and jamming into a single coherent architecture.

UAV Proliferation and Platform Diversification

The explosion in UAV deployment — from theater-level ISR assets to combat drones and loyal wingman concepts — has dramatically expanded the addressable market for lightweight, low-SWaP (Size, Weight, and Power) RWR solutions. Traditional RWR systems were designed for relatively large platforms with ample power budgets; UAVs demand miniaturized equivalents that offer meaningful threat detection without compromising payload capacity or endurance. This requirement has catalyzed significant R&D investment in compact, software-defined receiver architectures capable of operating from small form-factor electronics modules.

Situational Awareness as a Strategic Imperative

Across all platform types, military operators have recognized that superior situational awareness is force-multiplying. RWRs that provide not just detection but precise geo-location of emitters, real-time threat prioritization, and automated cuing of countermeasures enable crews to focus cognitive effort on mission execution rather than self-protection management. This demand for richer, more actionable information is driving investment in advanced display technologies, improved human-machine interfaces, and AI-assisted threat assessment tools.

Technology Trends Reshaping the Market

Digital and Software-Defined Receivers

The shift to fully software-defined receiver architectures is arguably the most consequential trend in the market. By replacing dedicated hardware processing chains with flexible, field-programmable platforms, manufacturers can update frequency coverage, sensitivity parameters, and threat libraries through software alone — without hardware modification. This dramatically reduces lifecycle costs and ensures that fielded systems remain relevant as adversary radar technologies evolve.

AI-Assisted Threat Classification and Cognitive EW

Machine learning algorithms are being trained on large datasets of radar emissions, enabling RWR systems to classify threats with high confidence even in dense electromagnetic environments. Cognitive EW systems extend this further, allowing the RWR to autonomously modify its operating parameters — antenna gain, frequency windows, processing priorities — in response to the environment. The result is a system that becomes more effective with operational experience, adapting dynamically to electronic counter-countermeasures (ECCM) employed by adversary radars.

Network-Centric Integration

Modern RWRs are increasingly designed not just to protect a single platform but to contribute threat data to broader network-centric warfare architectures. Intercept data generated by one aircraft can be shared across a formation or even disseminated to ground-based commanders, constructing a real-time, collaborative picture of the electromagnetic order of battle. This interoperability with tactical data links — including Link 16, MADL, and emerging 5G-based military communications — is becoming a key procurement requirement.

Low SWaP Solutions for Small Platforms

As RWR technology migrates to helicopters, light attack aircraft, UAVs, and ground vehicles, the emphasis on miniaturization has intensified. Advanced chip-scale packaging, gallium nitride (GaN) receiver front-ends, and highly integrated monolithic microwave integrated circuits (MMICs) are enabling manufacturers to deliver meaningful threat detection capability in modules weighing as little as a few kilograms — a fraction of the weight demanded by legacy systems.

Key Players in the Defense Radar Warning Receivers Market

The global RWR market is served by a concentrated group of major defense electronics companies, each with deep domain expertise and established relationships with military customers.

BAE Systems occupies a leading position, supplying the AN/ASQ-239 suite for the F-35 and a wide range of EW systems for allied air forces. Its Systems Electronic Warfare division is among the most technically capable in the industry.

RTX (Raytheon) brings a comprehensive EW portfolio that spans RWR sensors, jamming systems, and fully integrated defensive suites. Its AN/ALR-69A digital RWR remains in wide service aboard multiple US and allied platforms.

Northrop Grumman has invested substantially in next-generation EW architectures, including cognitive and AI-enabled systems designed for future platform integration. Its EPAWSS (Eagle Passive/Active Warning Survivability System) program for the F-15 represents the state of the art in legacy platform modernization.

L3Harris Technologies supplies a broad spectrum of electronic support measures and is a key provider of RWR systems for rotary-wing platforms and ISR aircraft. Its focus on open-architecture, software-defined systems aligns with emerging procurement preferences.

Leonardo (Italy/UK) supports the Eurofighter Typhoon’s PRAETORIAN Defensive Aids Sub-System and supplies advanced EW solutions across European and export markets.

Saab integrates its own EW suite into the Gripen E, combining a sophisticated RWR with an active jamming system in a compact, cost-effective package — a model increasingly attractive to mid-tier air forces.

Elbit Systems is a significant supplier to numerous export markets, with advanced RWR and DIRCM solutions integrated on platforms operated across Asia, Africa, and Latin America.

Thales delivers the SPECTRA EW suite for the Rafale, one of the most capable fully integrated defensive suites currently in operational service.

Bharat Electronics Limited (BEL) represents the emerging significance of indigenous defense electronics, supplying RWR systems for the Tejas Mk1A and contributing to India’s ambition of domestic capability development for the Advanced Medium Combat Aircraft (AMCA).

Regional Market Dynamics

North America

North America remains the largest and most technologically advanced segment of the global RWR market, driven by US Air Force, Navy, and Army modernization programs. The continued expansion of the F-35 fleets, ongoing F-15EX procurement, and B-21 Raider development all carry significant EW system content. Congressional emphasis on EW as a strategic priority has sustained funding across multiple budget cycles.

Europe

European demand is growing rapidly, propelled by NATO burden-sharing commitments, the rearmament programs triggered by the Russia-Ukraine conflict, and ongoing procurement of Eurofighter Typhoon, Rafale, and Gripen E platforms. European defense consortia are also investing in next-generation EW under the European Defence Fund framework.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional segment, with India, South Korea, Japan, and Australia all pursuing ambitious air power modernization programs. India’s Tejas Mk1A integration with indigenous RWR technology and its planned AMCA program position BEL and DRDO as significant domestic suppliers alongside international partners.

Middle East

Sustained geopolitical tension, substantial defense budgets, and significant procurement of advanced aircraft — including F-35s for Israel and UAE, as well as Eurofighters for Saudi Arabia and Kuwait — underpin strong RWR demand across the Middle East region.

Challenges Facing the Market

Despite robust demand, the Defense Radar Warning Receivers market faces meaningful technical and programmatic challenges. The sophistication of modern threat radars — including low probability of intercept (LPI) systems and frequency-agile, waveform-diverse emitters — places relentless pressure on RWR detection and classification performance. Dense electromagnetic environments, with hundreds of emitters operating simultaneously, stress the processing capacity of even the most advanced systems.

Integration complexity and cost represent persistent obstacles, particularly for legacy platform upgrade programs where airframe space, power availability, and cooling capacity are constrained. Cybersecurity concerns have also grown substantially, as software-defined systems and networked architectures introduce new attack surfaces that must be hardened against adversary exploitation.

Future Outlook: Toward Intelligent EW Nodes

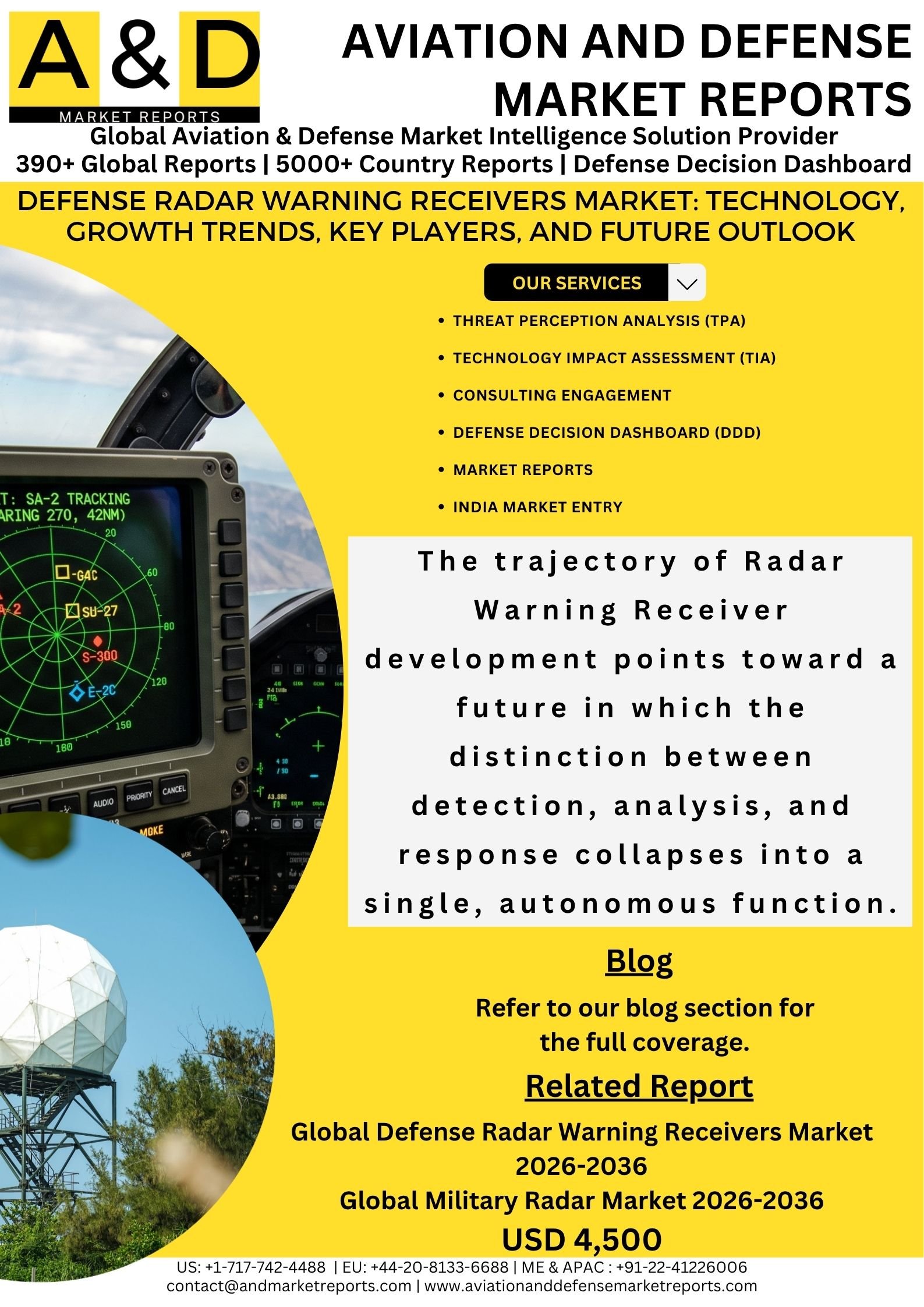

The trajectory of Radar Warning Receiver development points toward a future in which the distinction between detection, analysis, and response collapses into a single, autonomous function. Next-generation systems will not simply warn; they will continuously characterize the electromagnetic environment, autonomously select and execute countermeasures, and contribute to a shared electronic intelligence picture across the battlespace.

AI and machine learning will underpin this evolution, enabling systems to handle emitter environments that no pre-programmed library could adequately address. As quantum sensing and photonic technologies mature, they may further transform receiver sensitivity and frequency coverage. The RWR of 2035 will be less a warning device and more an intelligent electronic warfare node — an indispensable, adaptive component of the networked, multi-domain force that modern militaries are racing to field.

The Defense Radar Warning Receivers market stands at the center of this transformation: technically demanding, strategically essential, and driven by the enduring imperative of keeping aircrews and their platforms alive in an increasingly lethal electronic battlespace.